What the evidence says and recommendations for future research

Fast facts

Policymakers, regulators, stakeholders, and academics have yet to grapple with the full cross-sectional impacts of hospital mergers. While the evidence is clear that consolidation leads to higher prices in concentrated markets, evidence is mixed on how it impacts the communities in which it occurs, how consolidation affects healthcare providers subject to acquisitions, and how those providers’ patients are affected after mergers are completed. Answers to all these broad questions require further research. Despite these gaps, there is some evidence of the broad consequences of hospital consolidation. Among them:

- The consolidation of hospitals into larger systems can reduce competition, thereby strengthening the bargaining leverage of these hospital systems to command higher reimbursement rates (increased prices).

- When hospital mergers result in higher market concentration and decreased competition among healthcare providers, wages and local economies can suffer. Rural communities are particularly vulnerable to these effects.

- Healthcare providers, specifically nurses and pharmacy workers, are often subject to the negative effects of monopsony power—the power that monopolistic hospitals can exercise in local labor markets with increased market share due to consolidation—resulting in suppressed wages and decreased job mobility.

- Patients’ care options can become limited, resulting in lower quality or restricted geographic availability. Yet mergers also can result in an influx of financial support, leading to new lines of health services, access to a larger network of healthcare providers, and a wider or newer array of technologies for patients.

More evidence is needed to develop policies and models of antitrust enforcement that mitigate the harmful impacts of hospital consolidation while bolstering the positive consequences of these mergers. In areas where evidence is mixed or missing, this report recommends specific topics of investigation to researchers.

The U.S. hospital market is amid a wave of mergers and acquisitions that first began about 30 years ago and has accelerated steadily since 2010. This wave of merger activity, and particularly the recent acceleration in hospital consolidation, is due to various factors, including rising financial instability faced by hospitals, seeking stronger bargaining leverage in the face of increased consolidation in other healthcare sectors, establishing efficiencies and economies of scale, expanding services and care delivery, and a changing healthcare regulatory landscape.

When considering how to address hospital merger activity and its implications, researchers and policymakers alike must look to antitrust leadership and identify scholarship that best informs their work. The Federal Trade Commission is one of two federal antitrust agencies, along with the Antitrust Division of the U.S. Department of Justice, that handle federal antitrust reviews. State antitrust agencies also review hospital mergers for possible anticompetitive effects.

Currently, the Federal Trade Commission is emphasizing understanding of the root causes of unlawful conduct and taking a more interdisciplinary approach in terms of analytical tools and the integration of consumer protection and competition within the agency. This emphasis provides an opportunity for comprehensive analysis outside the scope of legal studies to inform the work of these agencies.

Policymakers, regulators, stakeholders, and academics, however, have yet to grapple with the full cross-sectional impacts of hospital mergers. While the evidence is clear that consolidation leads to higher prices in concentrated markets, evidence is mixed on how it impacts the communities in which it occurs, how consolidation affects healthcare providers subject to acquisitions, and how those providers’ patients are affected after mergers are completed.

Answers to all these broad questions require further research. Despite these gaps, however, there is some evidence of the broad consequences of hospital consolidation. Among them:

- The consolidation of hospitals into larger systems can reduce competition, thereby strengthening the bargaining leverage of these hospital systems to command higher reimbursement rates (increased prices).

- When hospital mergers result in higher market concentration and decreased competition among healthcare providers, wages and local economies can suffer. Rural communities are particularly vulnerable to these effects.

- Healthcare providers, specifically nurses and pharmacy workers, are often subject to the negative effects of monopsony power—the power that monopolistic hospitals can exercise in local labor markets with increased market share due to consolidation—resulting in suppressed wages and decreased job mobility.

- Patients’ care options can become limited, resulting in lower quality or restricted geographic availability. Yet mergers also can result in an influx of financial support, leading to new lines of health services, access to a larger network of healthcare providers, and a wider or newer array of technologies for patients.

More evidence is needed to develop policies and models of antitrust enforcement that mitigate the harmful impacts of hospital consolidation while bolstering the positive consequences of these mergers. In areas where evidence is mixed or missing, this report recommends specific topics of investigation to researchers. This includes answers to questions such as:

- Have there been any changes in the overall economic health of the local healthcare industry due to hospital consolidation?

- What impact has hospital consolidation had on the quality of care that clinicians, including doctors, nurses, and other healthcare professionals, can provide?

- Is there sufficient research on the impacts of hospital consolidation on various demographic populations and disease groups, and how may those activities exacerbate or improve disparities?

- How can policymakers ensure that hospital consolidation does not disproportionately impact vulnerable communities and rural populations?

This report will contribute to the growing body of evidence focused on the implications of increased market concentration of hospitals and health systems by creating an initial landscape of the existing research gaps and opportunities related to hospital consolidation. This report describes and contextualizes, through the market activities of hospitals and health systems, the positive and negative impacts of hospital consolidation on local economies, healthcare providers, and patients after mergers and acquisitions are completed.

In answering these questions, policymakers, stakeholders, and regulators then can appropriately target bad actors in the consolidation process and bolster policies that encourage healthy market dynamics while buffering local communities from any economic ill-effects, preserving provider autonomy and labor opportunities, and improving the quality of care and access for vulnerable patients. The result would be a more effective and efficient U.S. healthcare system, in turn helping ensure more equitable and sustainable economic growth.

The consolidation of hospitals across the United States has been markedly on the rise in the healthcare industry over the past few decades. The available evidence today indicates this consolidation is concentrating hospital markets and reducing competition.

There were 1,519 hospital mergers announced, though not all completed, in the past 20 years, with 680 since 2010. Now, more than 90 percent of Metropolitan Statistical Areas—the more than 400 geographic regions of the country associated with a core area of relatively high-density population—are considered highly concentrated for hospitals. Most of these areas are dominated by one large health system, such as what we see in Boston (Mass General Brigham), Pittsburgh (University of Pittsburgh Medical Center), and San Francisco (Sutter Health).

Research also demonstrates that monopoly pricing by hospitals—that is, prices at hospitals with no other hospitals in a 15-mile radius—are, on average, 12.5 percent higher than hospitals with three or more potential competitors nearby. Less research has examined the implications beyond price impacts of hospital consolidation and increased hospital market concentration on local economies, healthcare workforces, and patients’ access to healthcare and the quality of that care.

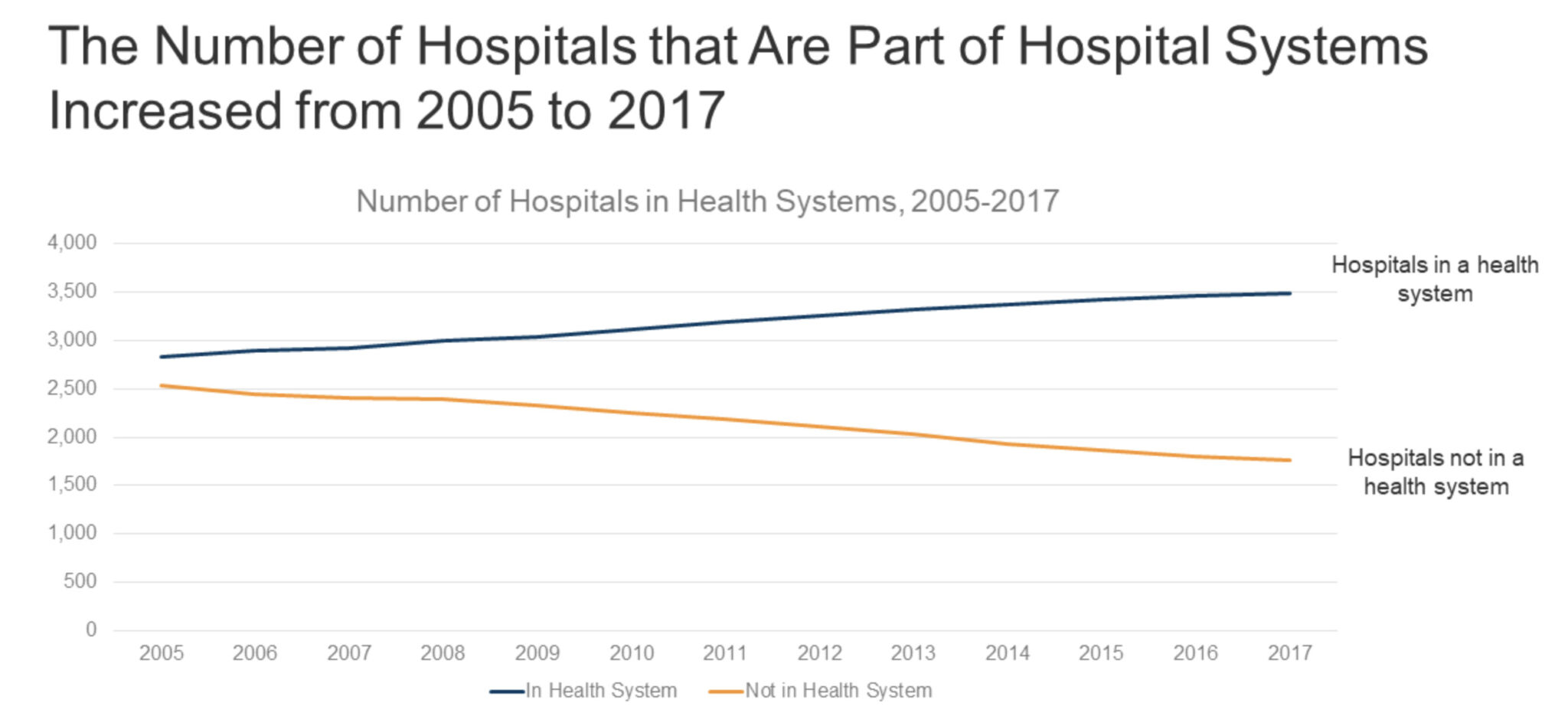

The past decade in particular is marked by significant shifts in how the hospital industry is organized and operates due to mergers and acquisitions of hospitals and independent physician practices and the expansion of monopolistic hospitals and health systems. Since 2010, the number of independent hospitals has declined due to mergers, while the number of hospitals that are part of larger systems has risen. (See Figure 1.)

Figure 1

As of 2017, 19 percent of markets—representing 11.2 million U.S. residents—were served by only one hospital system. These concentrated markets are susceptible to, or have already been impacted by, these shifts in market dynamics and subsequent changes in bargaining leverage exercised by consolidated hospitals and health systems on prices and local labor markets. Numerous studies have already found that consolidation is associated with high healthcare prices. This is important because healthcare prices in the commercial sector drive healthcare spending growth.

The United States, in 2021, spent $4.3 trillion on healthcare, significantly more than comparable peer nation members of the Organisation for Economic Co-operation and Development. This spending made up 18.3 percent of U.S. Gross Domestic Product in 2021 while large, wealthy peer countries averaged between 11 percent and 12 percent of GDP and the OECD average was 9.6 percent of GDP. This high spending in the United States does not improve the quality of care or access to care, compared to peer countries. Of that $4.3 trillion, hospital-related expenses account for $1.3 trillion, or 31 percent of domestic health spending (compared to an average of 28 percent among OECD countries), making up roughly 6 percent of U.S. GDP.

Considering how consolidation of hospitals and health systems can drive up prices for consumers and their health insurance premiums, studying and addressing the consequences of hospital consolidation is an essential part of containing healthcare spending and protecting healthcare purchasers from increased prices and other consolidation costs related to the quality of care and access to that care.

Two primary types of consolidation in the healthcare sector are the primary focus of academic and policymaker discussions: horizontal and vertical. More specifically:

- Horizontal consolidation refers to mergers among organizations operating at the same level in the healthcare supply chain. This happens when hospitals or health systems merge with other hospitals or when physician practices merge with other physician practices.

- Vertical consolidation refers to mergers among organizations operating at different levels in the healthcare supply chains. This happens when hospitals and health systems purchase or acquire physician groups, post-acute care facilities, behavioral health services, and other practices in the healthcare supply chain. We will not be focusing on this type of consolidation in this report except briefly in the case of the vertical integration of physician groups.

Both forms of consolidation can occur within a single market or across markets, in what are referred to as cross-market mergers. This report primarily focuses on horizontal hospital consolidation between hospitals and health systems, but also touches on the impacts of the vertical integration of physicians into hospitals and health systems as these forms of consolidation often co-occur in markets.

Hospital consolidation occurs in the United States for several reasons, sometimes in response to external pressures and other times due to internal business and service delivery decisions. Below are brief summaries the five most important drivers of hospital consolidation. While all of these are claimed motivators for consolidating, whether hospitals and systems achieve these intended goals post-merger is yet to be determined.

Financial stability

Consolidation can help struggling hospitals improve their financial stability by reducing operating costs and achieving economies of scale. In this way, a merger can save a hospital or a physician’s practice. According to hospital leaders, the benefits of mergers include cost reductions related to the scale of hospital operations, which allows the dispersal of expenses across a larger patient population, lowers the cost of capital, and provides savings from the standardization of clinical processes.

Increased bargaining leverage

Consolidation can bolster hospitals’ bargaining leverage with increasingly consolidated health insurance companies. By increasing their bargaining leverage, health systems can secure more favorable contract terms, such as selection by an insurer as a covered provider or higher reimbursement rates.

Efficiencies and economies of scale

Hospitals affiliated with larger systems can have increased access to shared staff and other administrative resources, helping to lower and spread fixed costs. An American Hospital Association analysis found that hospital acquisitions are associated with a 3.3 percent reduction in annual operating expenses per admission at acquired hospitals. Some other industry studies suggest that, depending on implementation, these cost reductions could reach 15 percent to 30 percent due to economies of scale.

Expansion of services, care delivery, and coordination

Consolidation can allow hospitals to expand their services and offerings to meet the needs of their communities. Post-acquisition analysis shows that 38 percent of acquired hospitals have added at least one service. These expansions can lead to improved care coordination and integration of services, resulting in higher-quality patient care.

Response to changes in regulatory and payment environment

Consolidation can help hospitals respond to changes in the healthcare regulatory landscape, such as the implementation of the Affordable Care Act and other shifts toward value-based payment systems aimed at improving quality and reducing costs, such as shared savings programs, episode-based payments, and global budgeting. By sharing administrative and financial burdens across more sites of care and larger population pools, the hope is to leverage those features to make implementation of policies or participation in programs easier.

How policymakers are responding to hospital consolidation

Several pieces of legislation have been introduced at the federal and state government levels over the past 10 years to promote healthcare competition, correct market distortions, and to ensure the benefits that hospital leaders tout about consolidation are not accompanied by corresponding ill-effects. In 2023 alone, states enacted at least 36 bills across 24 states related to health system consolidation and competition. Two of the most significant focus areas at the state and federal levels are:

- Financial and price transparency, which includes state legislative and congressional proposals and state and federal administrative actions to promote hospital price transparency, prevent surprise medical bills, and encourage the shopability of medical services based on prices

- Antitrust enforcement, includingstrengthening state and federal antitrust laws and enforcement efforts on anticompetitive conduct and efforts to tighten merger oversight in the healthcare sector

The effectiveness of these measures varies depending on political and economic conditions, the size and scope of the healthcare industry in each market, and the resources available for federal and state enforcement. The next section of this report examines in greater detail what is sparking these legislative and administrative actions.

The consequences of hospital consolidation are nuanced and depend on various factors, such as certain market characteristics, healthcare provider specialties, and patients’ many and varied characteristics. This section provides an overview of the general effects observed from hospital consolidation. I then more deeply explore what is known about how hospital consolidation affects three particular areas:

- Healthcare labor markets, including the effects on clinicians’ wages, the availability of jobs, and the unique role rural hospitals play in their communities

- Healthcare providers’ professional autonomy, job security, compensation, , the quality of care they can provide to patients, and how nurses exemplify the confluence of consolidation issues affecting all healthcare providers

- The affordability, quality, and accessibility of healthcare services for patients with a spotlight on obstetrics services

Overview of the impacts of hospital consolidation

Before examining the potential downsides of hospital consolidation, it must be acknowledged that consolidation also can deliver considerable benefits. Positive outcomes from hospital consolidation include:

- Financial stability and operational efficiencies. Mergers and acquisitions are tools that some health systems use to keep financially struggling hospitals open by averting bankruptcy or closure. This is in part because newly affiliated hospitals may have more ability to tap into available resources from the system compared to independent hospitals.

- Increased services. Partnerships, mergers, or acquisitions can help create more cohesive care. Research shows that nearly 40 percent of hospitals affiliated with a consolidated health system added one or more services post-acquisition. These improvements make it easier for patients to access specialists or services originating in the acquiring system and can help to ensure that care remains in the community.

- Community engagement. Some researchers observe greater community engagement for system-affiliated hospitals than their independent counterparts.

Consolidation is not inherently bad, nor should it necessarily be discouraged. What researchers and policymakers need to be concerned about are the negative outcomes that arise from abuses of market power when these hospital mergers and acquisitions occur in already-concentrated markets, leading to further reduced competition. This reduction in competition has been associated with negative consequences, such as increased healthcare prices, lower quality of care, and reduced access to care. These impacts are discussed in greater detail later in this report, but let’s briefly detail them here.

Increased prices

The consolidation of hospitals into larger systems can reduce competition and increase concentration, thereby strengthening the bargaining leverage of these hospital systems to command higher reimbursement rates (increased prices) from private payers.

Hospitals and systems with market power resulting from consolidation have greater leverage to raise prices in insurer negotiations. Research shows that hospital mergers can increase commercial sector prices by an average of 6 percent, with even more significant price increases in areas with higher market concentration.

Even when a hospital merges with a hospital in a different geographic area or market (a cross-market merger), evidence suggests there are price impacts. One analysis finds that prices at hospitals acquired by out‐of‐market hospital systems increased by about 17 percent more than their peer unacquired, stand‐alone hospitals. A reason for these price increases is that even in a cross-market merger, the hospital has improved its bargaining positions with insurers. Insurers are trying to operate in large geographic areas with large provider networks since it makes them attractive to employers who operate in multiple markets. This large geographic span usually benefits them in negotiations with hospitals, but when the health systems expand their reach, insurers lose their leverage and prices can increase.

Increased prices for patients also can originate from large hospital systems shifting their patient volume to higher-cost care treatments or facilities. For instance, pre-merger or pre-acquisition patients might have been receiving treatment in their local physician’s office, but once the physician is employed by the hospital, they receive their care at a hospital outpatient facility. Their care and their physician have not changed, but the amount insurance or the individual will be billed increases due to the new site of care being a more complex facility than the physician’s office. This is more often brought up as an incentive and driver of vertical consolidation.

Wage stagnation

With healthcare costs rising more rapidly in recent years, there is growing concern that the increase in healthcare spending crowds out wage growth and that hospitals in concentrated markets can use their market power to suppress wages. This has been most clearly studied as it applies to nurses’ wage suppression in concentrated hospital labor markets and will be discussed in greater detail later in this report.

Closures of hospitals and lines of service

When large health systems acquire hospitals, they may close or eliminate select service lines. Large hospital systems with multiple care sites can shift volume to higher-cost facilities, leading to higher prices. Closures also can be based not on community needs but on corporate business considerations that favor other hospitals in their system over the ones they closed. Often, there is little or no local consultation or public input process before hospital consolidations happen.

Improving or declining quality of care

Evidence is not conclusive or consistent on the association between hospital mergers and the subsequent quality of care. The quality effects of consolidations differ depending on the role of the hospitals in their communities and the measures used to assess that quality, including mortality, readmissions, complications, clinical processes, and patient experiences.

Increased profits and the use of those profits

Sometimes, consolidation can increase hospital profits as larger healthcare systems achieve operational efficiencies and use their leverage to extract higher prices from insurance company payers and hospital suppliers. Yet the impact of consolidation on hospital profits and savings can vary depending on a range of factors, including the specifics of the merger, the size of the resulting healthcare system, and the local market conditions. Research has found that when cost efficiencies are measured, they are modest, at less than 5 percent.

Importantly, however, evidence suggests that the impacts of hospital consolidation can vary depending on the profit status (for-profit vs. nonprofit) of the hospitals involved. Recent research finds that as market competition decreases, the distribution of Medicaid admissions shifts away from nonprofit hospitals to public hospitals, potentially straining facilities that serve large numbers of uninsured and Medicaid patients.

Reasons for these differences originate in the priorities and incentives of hospitals based on their financial structures. For-profit hospitals may prioritize financial outcomes and implement cost-cutting measures to improve performance. This can lead to the closure of “underperforming” facilities within the hospitals, such as low-volume obstetrics, and compromise the quality of care. The prioritization of finances and centralization of care away from local hospitals can disproportionately affect rural areas where hospitals are already more likely to experience financial challenges or be the sole providers of care.

Hospital consolidation’s impacts on local labor markets

The study of local labor markets in the United States when discussing hospital consolidation is essential because local hospitals are often one of the largest employers in communities, and changes to their employment patterns can impact their local communities economically. These effects on employment and wages can extend from clinicians to nonskilled labor, and even to those outside the employment of hospitals, through increased healthcare prices and their subsequent impacts on business and household budgets.

The concentration of labor markets as a driver of wage stagnation for certain clinicians is supported by a growing body of evidence, with a documented negative correlation between hospital consolidation and wages. This evidence on the consequences of the exercise of labor monopsony by merged hospitals and hospital systems can help inform antitrust authorities as they evaluate mergers and propose regulatory mechanisms to curb consolidation that results in increased market concentration. So, let’s look at the several ways in which local markets are affected by hospital consolidation.

Hospital consolidation suppresses wages and employment of clinicians and other staff

Trends in hospital consolidation have increased concerns about the effects on clinicians’ wages, including physicians, nurses, and other healthcare specialists. While concern spans all specialties and positions, market concentration in the hospital industry has resulted in stagnant or declining wage growth for nurses and pharmacy workers in particular. When hospitals increase their share of the local labor market for clinicians, they gain leverage in employee negotiations. This enables some consolidated hospitals to suppress the wages of certain employee groups despite increasing prices.

These wage effects have been felt more acutely by some clinicians based on their specialty, as previously mentioned, but also based on their geographic location. When looking at merger-wage effects in rural areas, some hospitals have decreased their spending on employee salaries, cutting their budgets by as much as $664,488, or $1,223 per full-time equivalent employee. But it is unclear whether these decreases reflect gained efficiencies, changes in staffing mix, or other operational decisions or if they are reflective of the exercise of market power to reduce wages or hours.

In addition to wage effects, consolidation may result in job losses and reduced job security via standard post-merger business activities, such as the integration of administrative functions, the elimination of duplicate positions, and changes in staffing ratios. This can be viewed as a positive from the business side of things if these actions are correcting for financial struggles but are a negative for those workers whose jobs have been reduced or eliminated due to a merger or acquisition.

Hospital consolidation suppresses wages and employment outcomes beyond the healthcare sector

The scale of the hospital sector in the United States is enormous, accounting for $1.3 trillion of healthcare spending and continuing to grow more rapidly than other healthcare sectors, including physician and clinical services and prescription drugs. Higher hospital prices impact the local communities they serve economically through the costs of health insurance coverage. More than 150 million U.S. workers receive health insurance benefits from an employer as compensation. The average cost of family coverage has only continued to increase over the past decade. In 2022, it was $22,463 for a family—of that, $6,106 was paid by the worker and $16,357 by the employer. (See Figure 2.)

Figure 2

There continues to be concern that increased spending on health insurance premiums by employers crowds out wage increases. When employers face increasing healthcare costs, these costs are often covered by increased insurance premiums paid by employees or by a lack of wage growth to offset those expenses. These premium price effects are more acutely felt by workers who receive employer-sponsored insurance in a local market where hospital mergers have resulted in a more concentrated market. Ultimately, workers are double-dinged when their wages go toward increased premiums and then they become purchasers of higher-priced care in a concentrated hospital market.

As researchers look further into the consequences of hospital consolidation on local economies, they can think about them as internal impacts to the hospitals themselves and external impacts to the communities in which they operate. Take hospital employment practices as an example. As discussed above, hospital consolidation can internally impact hospital employees through employment status or wage changes and then externally impact nonhospital employees through the effects of higher healthcare prices and heftier health insurance premiums.

Further research questions for consideration include where and to whom costs are passed in local markets following hospital mergers, how the consequences in terms of economic growth may vary by market demographics, and if there are trends due to location, particularly any interactions with nearby economically homogenous or affluent areas. Understanding changes to hospital revenue generation pre-and post-merger, and then how profits and capital are used post-merger, needs to be an increasingly integral part of understanding the broader landscape of hospital consolidation. These analyses should factor in market and demographic differences based on population and payer characteristics, such as race, age, income, disease burden, and public vs. private payer mix.

Hospital consolidation’s impacts on healthcare providers

In 2019, there were 22 million workers in the healthcare industry, employing 14 percent of all U.S. workers. Given the size and scale of the healthcare sector, the consequences of consolidation on its clinicians and other workers warrant attention by policymakers and researchers. Beyond the impacts on wages discussed above, this section outlines how consolidation affects employment opportunities and job satisfaction among hospital staff. These factors can significantly impact the quality of care and subsequent patient outcomes, making it critical to address the potential consequences of hospital consolidation.

Physicians

The trend toward consolidation affects physicians as they are subject to ownership changes at hospitals they already work for or end up encouraged to vertically consolidate their practices with hospitals and health systems. While this report has thus far focused on the horizontal consolidation of hospitals and their impacts, the story of hospital consolidation would not be complete without a brief discussion of the vertical consolidation of healthcare providers—particularly physicians—and their subsequent experiences in merged hospitals and health systems.

The vertical consolidation of physicians into hospitals and systems has increased in the past decade, with 2016 being the first year in which fewer than half of practicing physicians (47.1 percent) had an ownership stake in their practice, and with 2018 marking the first year in which there were fewer physician owners (45.9 percent) than employees (47.4 percent).

This decline in physician ownership will continue as more physicians become vertically integrated or employed by hospitals or health systems. This trend has significant implications for the healthcare industry, as physicians employed by hospitals may be subject to different incentives, priorities, and administration burdens and barriers than those who are self-employed or part of smaller practices.

Unfortunately, our understanding and evidence of clinician well-being and job satisfaction mostly come from convenience samples and surveys from voluntary hospitals and health systems, and often from only physicians or only nurses. Even with those measurement challenges, we should pay some attention to the impacts of hospital consolidation on clinician job satisfaction, as burnout and job dissatisfaction can lead to poor patient outcomes and exacerbate clinician shortages.

It is also worth noting that while not formally investigated yet, all these effects of consolidation on physicians may be compounded by the impacts of the COVID-19 pandemic. Evidence shows that the pandemic decreased job satisfaction among healthcare providers. It also decreased employment, with hundreds of hospital-based physicians experiencing furloughs or layoffs when elective surgeries were paused, causing procedural and revenue decreases for hospitals and health systems. The COVID-19 pandemic may spur additional research in this space at a time when evidence and policy are greatly needed.

Nonclinical hospital staff

The impact of hospital consolidation on all hospital staff, including nonclinical staff, is crucial for evaluating the broader implications of consolidation in the healthcare industry and local economies, where health systems can comprise a large portion of employment.

Nonclinical staff are more insulated from the impacts of hospital consolidation

As previously discussed, hospital consolidation can impact staffing levels and thus job security, compensation and benefits, and the overall work environment. But nonspecialized workers, such as custodians, food-service workers, and security guards, are less likely to be affected by a merger since their skills are transferable to employers in other sectors, assuming availability in their local market and that the hospital is not the dominant employer in their field of work. Excluding that dominant-employer scenario, hospital consolidation has not been found to depress the wages of general or blue-collar workers whose skills are not industry specific.

However, while nonclinical staff may be protected from wage effects, their job satisfaction and subsequent responses may still be positively or negatively impacted by consolidation, similar to clinical staff, when there are changes to workloads or processes. For this reason, further inclusion of all hospital employees in impacts analysis is needed.

Ultimately, hospitals are in the business of providing care, so studying and understanding the consequences of hospital consolidation on the individuals they employ to provide that care is important. Questions for consideration include how the availability of resources and support for clinicians changes pre- and post-merger, how autonomy changes and then affects clinical care decisions, and whether changes in caseloads impact care delivery and job satisfaction.

Regarding the clinician-patient relationship and how hospital consolidation can affect it—with a particular eye on issues of health equity and clinician diversity—researchers should investigate the impacts on continuity of care under ownership changes and the availability of specialists and clinicians of diverse backgrounds.

Hospital consolidation’s impacts on patients

Much of the discussion in academic literature and among policymakers has focused on the impact of consolidation by way of induced price increases on household budgets while placing the patient at the periphery instead of the center of the issue. A reason for this divorce in focus lies in the difficulty of measuring how hospital consolidation and market concentration can impact patients’ quality of care and access to that care.

Despite this challenge, some compelling research does examine patients’ quality of care and access to care. So, let’s briefly look at what evidence is available on the effects of prices and then on quality and access for patients to demonstrate this area is ripe for further investigation.

Prices

The growth in hospital prices is the major driver of healthcare spending growth in the commercial sector, and healthcare spending consumes a growing share of U.S. individual and family budgets, leaving less to spend on other necessities. Additionally, as previously discussed, rising healthcare spending is associated with wage stagnation, compounding the issue of rising expenses with reduced or suppressed income. This combination of increased costs and the stress it produces on families’ budgets and well-being makes it necessary to examine both the household effects of rising prices on patients and the care outcomes they are often over-paying for.

Increased prices after hospital mergers in concentrated markets do not always result in improved mortality or investment in care

Understanding the interplay between prices and the quality of care in hospitals has proven to be a moving target for researchers to measure, given the difficulty of controlling for external influences on outcomes and how that in turn factors into the creation of quality measures.

Higher nominal prices are not necessarily bad when patients get more value for their money in the form of improved outcomes, more easily measured in the form of mortality rates. The question of whether higher priced care is better care remains unclear, but in cases where improvements in mortality rates are gained at higher-priced hospitals, it only holds true in less concentrated markets. This could be in part because the increased spending to deliver a higher quality of care would help a hospital distinguish itself from competitors. In concentrated markets, research shows no effect on mortality, even when spending increases. It is not always clear what this spending goes toward and it may not be on activities that increase outcomes in the absence of a competitor to compete with on quality.

Hospitals’ increasing spending without measurable improvements indicates a broken market where hospitals should compete on costs and quality. When hospitals no longer need to compete on that basis, their incentives to provide higher-quality care or invest in innovations and technologies can be affected. This can manifest as decreased financial investment in low-profit-generating initiatives, such as quality improvement or social determinants of health interventions.

Quality and access

Hospital consolidation in the United States has complex and multifaceted effects on the quality of care. There is a growing body of mixed evidence on the impacts of care pre- and post-merger, demonstrating the complexity in capturing quality impact. Factors such as the specifics of the consolidation, the size of the resulting healthcare system, types of hospital units effected, and changes over time all contribute to these varied outcomes that require further exploration.

Acquired hospitals may benefit from increased resources offered by their new system improving patient access and choice

Mixed evidence suggests consolidation can lead to improved coordination of care, better management of complex medical conditions, and reduced readmissions, contributing to enhanced quality of care. In many cases, though, a positive action can eventually lead to a negative outcome, so discerning where in the process of consolidation and market concentration the issue arises can help better target policy and regulation.

For example, integration of healthcare institutions can advance the dissemination of best practices and treatments, improving hospital performance and patient outcomes. However, increased network communication and shared learning does not always mean the “best” practices are being disseminated or encouraged. Following this thread, we see evidence that consolidation into large healthcare systems within highly concentrated markets can lead to overtreatment. This is due to the lack of competition creating financial incentives to recommend unnecessary tests and procedures. In addition to the concerns around the quality of care associated with unnecessary and low-value services, this also has negative implications for healthcare spending through overutilization.

On the flip side, when actual best practices are shared, mergers and acquisitions of physician partnerships help improve access to care for patients in rural and underserved communities. These mergers can enable hospitals to expand service offerings, broaden provider and specialist networks, and better serve patients in their local communities.

Quality of care after hospital consolidation is not sufficiently studied, especially among specific patient groups and geographies

While there may be some efficiency benefits from mergers and acquisitions, the impact on patient outcomes, particularly for different disease groups, should be central to any discussion. Research has yet to demonstrate the definitive benefits of consolidation via improved quality.

Given their complexity and vulnerability to noise, analyses of quality measures tend to be narrowly focused on geographies, disease groups, or other populations where variables can be better controlled for. For instance, researchers find a decrease in mortality among patients staying in the hospital for acute myocardial infarction, heart failure, stroke, and pneumonia post-merger at merged rural hospitals, compared to those that did not merge. While this evidence is great, it is limited to those diseases and rural hospitals. These nuanced studies are important to understanding the full scale of impacts, but many more are needed to build the evidence base.

When quality is studied post-merger in a broader population, often those studies are older in origin and there are little to no improvements found and, in some cases, there are worse outcomes or changes in practice patterns that are associated with worse or unnecessary care. For example, mergers in California between the years of 1990 and 2006 have been shown to increase the likelihood of intensive surgery and the total number of surgeries performed while not improving patient outcomes.

Another outdated study in need of a refresh tracks Medicare patients who had heart attacks between 1985 and 1994 in more concentrated markets, finding that their risk-adjusted 1-year mortality rate was 4.4 percent higher, compared to those patients in less concentrated markets. Both of these studies demonstrate the valuable evidence that can be generated from these analysis on consolidation impacts on quality and highlight the need for more.

On a final note, consolidation also is associated with a small decline in patient experience measures. While these experience measures are not of as high importance as others such as mortality outcomes and are self-reported patient experience can still serve as a metric for overall hospital performance.

All stakeholders in the U.S. healthcare system, including patients, healthcare providers, payers, and policymakers, need to consider how to maintain or create competitive markets that produce high-quality and equitable care. This requires evidence on the full scope of effects of hospital consolidation on pricing and the quality of care and access to care.

As put forth in this report, there are several detailed questions that must be considered and answered. This includes considering hospital consolidation that occurs within and outside of concentrated markets as the impacts can be expected to vary in more concentrated versus less concentrated markets. Longitudinal approaches would also be beneficial applied to all the areas of research outlined below.

How can we better estimate the local economic impacts of consolidation beyond price and wage effects?

While the price effects of consolidation are known, taking these analyses further to explore how they impact specific populations or market subsects and under different payer mixes would be extremely valuable in developing public and private payment policies and systems of integrated care. Specifically:

- To whom and in what proportion are the price increases following hospital consolidation passed on to insurers, patients, employers, or taxpayers?

- How can antitrust policymakers better estimate the local economic impacts of consolidation beyond the effects on prices and wages?

- Does consolidation reduce or encourage economic growth? Does this vary by market or population characteristics?

- Are consolidation and increases in market concentration more likely to occur in economically, racially, geographically, or culturally homogenous areas, compared to heterogenous communities?

- How are increases in capital or profit used post-merger? Can subsequent correlations be identified in terms of wider economic or community benefits?

What impact does hospital consolidation have on clinicians’ abilities to provide quality care?

As previously discussed, capturing the experiences of clinicians is already difficult without adding the lens of consolidation to the analysis. But there is room for improvement and pertinent questions to be contemplated, which would be helpful in the development of thoughtful policy and regulations related to hospital consolidation. Specifically:

- Does hospital consolidation lead to changes in the availability of resources and support for clinicians?

- Does hospital consolidation affect the autonomy of clinicians in making clinical decisions?

- Do clinicians experience changes in workload or patient caseloads?

- Do clinicians experience changes in the continuity of care or relationships with their patients due to hospital consolidation?

- What is the clinician’s perspective on the job market and opportunities for their specialty pre- and post-merger?

- Are there trends in specialist employment or geographic relocation of specialists following mergers or acquisitions? Are these associated with any patterns of clinician shortages?

- What is the uptake of new technologies that enhance clinician reach in hospitals pre- and post-merger or compared to independent hospitals?

How does hospital consolidation affect access to care and the quality of care for patients?

Measuring health outcomes is difficult, yet attempts to understand the consequences of hospital consolidation on specific demographics and disease groups are essential to building safeguards and targeted solutions into policies and regulations. In particular, the extent to which hospital consolidation contributes to disparities in access to healthcare for disadvantaged and minority populations remains unexplored. Specifically:

- Does consolidation reduce or expand locations or specific services more often than others? Are there trends where these service lines are affected?

- What impact does hospital consolidation have on the ability of patients to make healthcare decisions that align with their personal preferences and values?

- What are the impacts of patient access to culturally competent providers of varying demographics, such as age, race, languages, and gender?

- Does reduced competition and increased market concentration of hospitals worsen or improve financial barriers to care for minority and rural populations?

- Does consolidation exacerbate or remove barriers to geographic access to care?

Patients must rely on the hospital sector when they are most vulnerable, such as during acute illnesses, major injuries, or giving birth. In addition to being essential providers of care, hospitals are large employers with far-reaching impacts in their communities. Given their importance, policymakers and researchers must do more to understand the underlying causes of hospital consolidation and mitigate the potential negative impacts of hospital concentration in noncompetitive markets.

A healthy healthcare ecosystem is essential for patients and critical to the healthcare workforce and local economies. By prioritizing the preservation of competition, transparency of merger and acquisition activities, and equitable access to care, policymakers and researchers can help create a healthcare system that benefits all stakeholders and improves health outcomes for all patients.

Amy Phillips is a policy analyst for markets and competition policy at the Washington Center for Equitable Growth. Her areas of focus include hospital consolidation, healthcare market competition, health equity, and healthcare pricing and payment. Prior to joining Equitable Growth, she was a graduate fellow at Sirona Strategies, where she worked on two healthcare coalitions focused on acute care in the home and social determinants of health. Phillips also conducted health policy research in the office of Rep. Lloyd Doggett (D-TX) focused on telehealth and Medicare policy. She also served as the healthcare chief of staff at Arnold Ventures and was a research assistant at the Medicare Payment Advisory Commission, conducting research on a wide range of Medicare payment policy issues. Phillips received her Master of Public Affairs from the LBJ School of Public Affairs at the University of Texas at Austin and her B.A. in medical anthropology from the University of Pennsylvania.

This work was supported by Arnold Ventures. The Washington Center for Equitable Growth maintains full editorial control over all of its self-published pieces.

Felecia Phillips Ollie DD (h.c.) is the inspiring leader and founder of The Equality Network LLC (TEN). With a background in coaching, travel, and a career in news, Felecia brings a unique perspective to promoting diversity and inclusion. Holding a Bachelor’s Degree in English/Communications, she is passionate about creating a more inclusive future. From graduating from Mississippi Valley State University to leading initiatives like the Washington State Department of Ecology’s Equal Employment Opportunity Program, Felecia is dedicated to making a positive impact. Join her journey on our blog as she shares insights and leads the charge for equity through The Equality Network.

When some one searches for his essential thing, thus he/she desires

to be available that in detail, therefore that thing is maintained over here.

Hello colleagues, its impressive piece of writing concerning tutoringand fully explained,

keep it up all the time.